Getting The Home Renovation Loan To Work

Getting The Home Renovation Loan To Work

Blog Article

9 Simple Techniques For Home Renovation Loan

Table of ContentsThe Facts About Home Renovation Loan UncoveredRumored Buzz on Home Renovation LoanHome Renovation Loan Things To Know Before You BuyNot known Details About Home Renovation Loan The 5-Minute Rule for Home Renovation Loan

Numerous industrial banks provide home improvement loans with very little paperwork requirements (home renovation loan). The disbursal process, however, is made easier if you get the lending from the very same bank where you previously got a finance. On the other hand, if you are getting a loan for the very first time, you have to repeat all the steps in the funding application procedureThink about a residence restoration financing if you want to remodel your house and provide it a fresh appearance. With the help of these loans, you might make your home more visually pleasing and comfortable to live in.

The main advantages of making use of a HELOC for a home restoration is the versatility and reduced prices (normally 1% above the prime rate). Furthermore, you will only pay passion on the amount you take out, making this a good choice if you need to pay for your home restorations in stages.

See This Report on Home Renovation Loan

The major negative aspect of a HELOC is that there is no set settlement timetable. You have to pay a minimum of the passion every month and this will increase if prime rates rise." This is an excellent funding choice for home restorations if you wish to make smaller sized monthly settlements.

Offered the potentially long amortization duration, you might wind up paying substantially even more passion with a home loan refinance contrasted with other funding alternatives, and the prices connected with a HELOC will certainly likewise apply. A home mortgage re-finance is properly a brand-new mortgage, and the rate of interest could be greater than your existing one.

Prices and set up costs are commonly the like would certainly spend for a HELOC and you can repay the car loan early with no charge. Several of our consumers will certainly begin their remodellings with a HELOC and after that switch over to a home equity car loan once all the costs are validated." This can be a good home restoration funding option for medium-sized projects.

Not known Facts About Home Renovation Loan

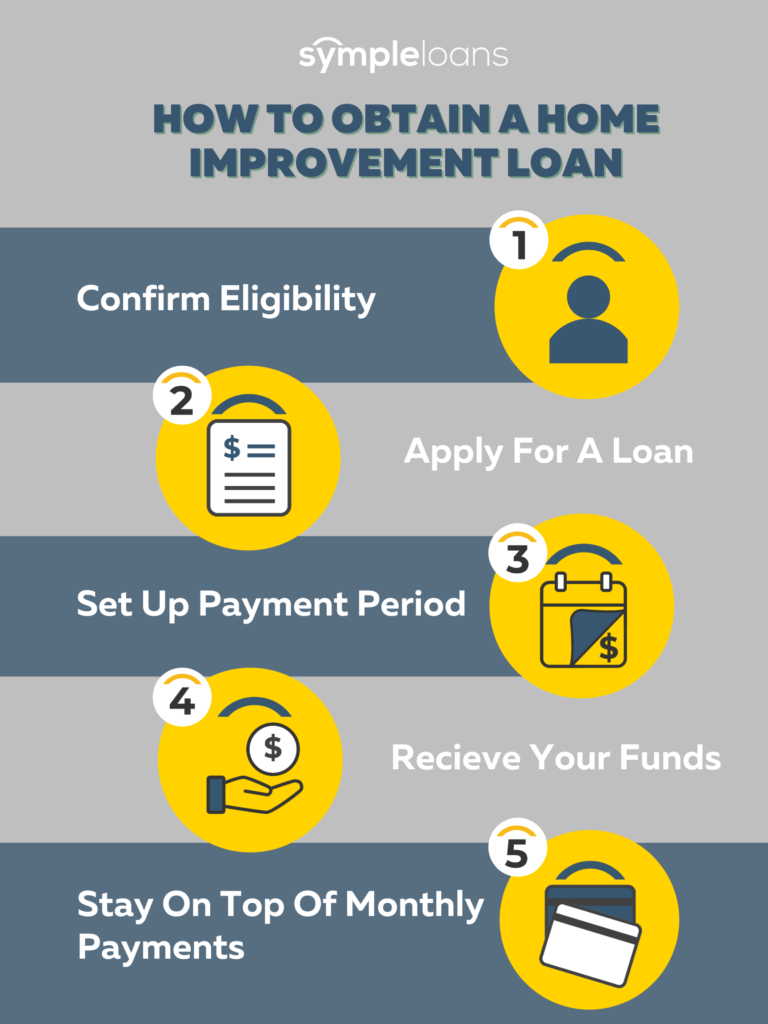

Home improvement loans are the financing alternative that permits homeowners to refurbish their homes without having to dip into their cost savings or splurge on high-interest bank card. There are a range of home improvement loan sources available to choose from: Home Equity Line of Credit History (HELOC) Continue Home Equity Car Loan Mortgage Refinance Personal Lending Charge Card Each of these funding alternatives includes distinct needs, like credit report, owner's income, credit line, and rates of interest.

Before you take the dive of creating your desire home, you most likely need to know the numerous kinds of home remodelling car loans available in Canada. Below are several of the most typical sorts of home remodelling loans each with its very own collection of qualities and benefits. It is a sort of home enhancement finance why not try this out that enables homeowners to obtain a bountiful amount of money at a low-interest price.

Facts About Home Renovation Loan Uncovered

To be qualified, you must have either a minimum of at least 20% home equity or if you have a home loan of 35% home equity for a standalone HELOC. Re-financing your mortgage process entails replacing your current home loan with a new one at a reduced price. It decreases your monthly repayments and reduces the quantity of passion you pay over your lifetime.

Nevertheless, it is very important to discover the potential threats related to re-financing your mortgage, such as paying a lot more in interest over the life of the finance and costly charges varying from 2% to 6% of the finance amount. Individual loans are unsafe loans finest suited for those who require to cover home remodelling expenses promptly however do not have enough equity to get approved for a protected loan.

For this, you might require to give a clear construction this content plan and allocate the restoration, including determining the price for all the products called for. Additionally, personal financings can be secured or unsecured with much shorter repayment periods (under 60 months) and come with a greater rates of interest, depending upon your credit rating and income.

Nevertheless, for small residence restoration ideas or incidentals that cost a couple of thousand dollars, it can be an appropriate alternative. If you have a cash-back credit card and are waiting for your following paycheck to pay for the acts, you can take benefit of the credit rating card's 21-day elegance period, during which no interest is accumulated.

The Definitive Guide for Home Renovation Loan

Shop financing programs, i.e. Store credit rating cards are supplied by lots of home enhancement shops in Canada, such as Home Depot or Lowe's. If you're preparing for small-scale home enhancement or do it yourself jobs, such as setting up new home windows or washroom remodelling, obtaining a shop card through the store can be a very easy and fast process.

Nevertheless, it is necessary to review the terms and conditions of the program carefully before deciding, as you might be subject to retroactive interest costs if you fall short to pay off the equilibrium within the time period, and the rate of interest rates might be greater than regular home loan funding.

Report this page